Faq : Investing

WHAT WE DO

- Offer investment advice or recommendations

- Guarantee any particular investment outcome

- Speak to investors about the merits of any particular company or offering

- Select which Issuers to list on our platform, by among other things:

- Conducting background checks on the issuer and its principals

- Conducting due diligence to have a reasonable basis for believing the issuer is complying with all its obligations

- Conducting due diligence to have a reasonable basis for believing the issuer has established a means to keep accurate records of the holders of its securities

- Advise Issuers about their offerings, and help prepare offering documents

- Screen investors to ensure that they satisfy applicable per-investor limits (discussed below)

- Provide communication channels between you and the Issuer, and between you and other potential investors, where you can ask questions and exchange information

- Provide search functions or other tools for investors

- Provide you with educational materials to help you assess the risks of investing (e.g., this document)

- Keep records of investor communications and materials

Issuers will pay us to be on our Funding Portal. They might pay us flat fees, commissions based on the amount of money they raise, or in other ways. They might also pay us for specified services we provide to them and reimburse us for expenses we incur on their behalf. For each offering you invest in, we will disclose our compensation.

In some cases, an Issuer might pay us in whole or in part with its own Securities, e.g., with its own promissory note. This will always be the same class of Security that is being offered to investors on our Platform. For example, if the issuer is offering common stock to investors, only common stock could be used for our compensation.

We will never own any financial interest in Issuers listed on our Funding Portal other than Securities we receive from them as compensation.

After an offering is complete, we might or might not have an ongoing relationship with the Issuer. The Issuer may decide to use our Funding Portal to raise money in the future, or use services provided by (and pay compensation to) entities affiliated with us.

We will maintain online communications channels –chat rooms, basically – where you can communicate with other investors and with the Issuer. All discussions on the chat rooms will be open to the public, but only investors who have registered with us are allowed to post. Representatives of the Issuer, and anyone engaged in promoting the offering, must clearly identify themselves as such. The chat room is where you can ask questions about investment opportunities that interest you.

We, the Funding Portal, generally aren’t allowed to participate in the chat room, except to establish guidelines and remove potentially abusive or fraudulent content.

WHAT YOU SHOULD CONSIDER FIRST

These definitions apply throughout this Investor Education Package:

Site – Our Internet site located at www.SmartMoney.inc.

Platform – Another word we use to refer to our Internet site.

Issuer – A company trying to raise money from investors on our Site, by selling its Securities.

Security – A share of stock, a promissory note, a bond, or any other instrument offered by an Issuer on our Site.

Title III – Title III of the JOBS Act of 2012, which allows “Regulation Crowdfunding.”

Funding Portal – A term used to describe Internet sites allowed to offer and sell Securities under Title III. We are a Funding Portal.

SEC – The U.S. Securities and Exchange Commission. The website: www.sec.gov.

FINRA – The Financial Industry Regulatory Authority. The website: www.finra.org.

Investing in the companies that will be offered on our Site is very different than investing in the public stock market. The companies at our Site are likely to be small, with limited or no track records and little profits, if any.

With those caveats, and even in view of the risks listed in the “Risks of Investing” section below, we believe that the companies on our Site will offer worthwhile opportunities both to invest in promising earn interest on your money and to invest in businesses you know and care about. With that said, what we believe doesn’t matter. The first thing for you to consider, before you go further, is whether it is appropriate for you to invest in any of these companies based on your own personal circumstances. Among the questions you should ask yourself are:

- Can I afford to lose all the money I invest?

- If I lose all or part of my money, will I be okay psychologically?

- Do I understand the company I am thinking about investing in? Do I understand its product or service? Am I personally familiar with that market?

- Do I understand the business the company is conducting? Do I understand how the company can make money?

- Do I understand the Security I’m buying?

- Do I trust the owners and managers of the company?

- Do I understand the documents I’m being asked to sign?

- Do I feel comfortable making this decision myself? If not, have I consulted with an advisor?

- Only if you can truthfully answer “Yes” to all those questions should you invest.

HOW TO INVEST

First, register at the Site. There, you will establish log-in credentials and provide us with some information about yourself.

You will also be asked to review and confirm that you will comply with our Terms of Use and Privacy Policy, and consent to electronic delivery (i.e., email) of all documents.

We have the right to reject or revoke your registration to our Site for any reason, including a violation of our Terms of Use or Privacy Policy.

Under Title III, the entire investment process happens online, through the Site. We will never send you paper, call you on the phone (except in some emergencies), or ask to meet with you.

Once we receive your investment commitment, we will notify you of:

- The dollar amount of your commitment

- The price of the Securities you committed to buy

- The name of the Issuer

- The date and time by which you may cancel your commitment

You can see investment opportunities as soon as you visit the Site. When you click on an opportunity that interests you, you will be able to see all the information available about the opportunity (see the “Issuer Information” section below). But you won’t be allowed to invest until you register.

Once you decide to invest, click on the “INVEST” button. We will ask for more information, arrange for you to pay for your investment, and asked you to sign one or more documents with the Issuer. For example, you might be asked to sign something called an “Investment Agreement.”

Having done all that, you will be deemed to have made an “investment commitment.” But you’ll still have a chance to cancel, as described below.

For each offering, the Issuer will disclose a “target offering amount,” meaning the minimum amount the Issuer is trying to raise (in some cases this could be as little as $1), and an “offering deadline.” If the Issuer doesn’t raise the target amount before the offering deadline, then the offering will be cancelled and any investors who have made investment commitments will receive their money back.

If the Issuer reaches the target offering amount before the offering deadline, it may close the offering early as long as (1) the offering has remained open for at least 21 days, and (2) we give a notice to investors. The notice must:

- Specify the new deadline, which must be at least five days after the date of our notice;

- Notify investors that they may cancel their investment commitment for any reason up until 48 hours before the new deadline; and

- Notify investors whether the issuer will continue to accept investment commitments during the 48 hour period before the new deadline.

If an Issuer intends to accept investments over and above the target offering amount, it must disclose the maximum amount it will accept and how it will handle “over-subscriptions.” For example, the Issuer might allocate the securities on a first-come first-served basis, or pro-rata among all of the investors who make investment commitments, or in some other way.

An investor must reconfirm his or her investment commitment within five days after a material change is made to an offering; otherwise, the investor's investment commitment will be cancelled, and the committed funds will be returned.

You will pay for your securities by a direct transfer from your bank account (an ACH transfer), which will be free to you.

When you invest, your money will be held in an account administered by a qualified third-party financial institution until the offering is completed. We, as a Funding Portal, are prohibited from holding your money. If the Issuer is successful in raising the target offering amount, the bank will release the investors’ money to the Company. We will notify you by email and the investment process will be complete.

Before your investment is final, we will send you a notice disclosing, among other things:

- The date of the transaction

- The type of Security you are buying

- The price and number of Securities you are buying, as well as the number of Securities sold by the issuer in the entire transaction and the price(s) at which the Securities were sold

- If you are buying a debt security, the interest rate and the yield to maturity calculated from the price paid and the maturity date

- If you are buying a callable security, the first date that the security can be called by the issuer

- The source, form and amount of any compensation we, the Funding Portal, expect to receive in the transaction

LIMITS ON HOW MUCH YOU MAY INVEST

If you are an “accredited investor,” you can invest as much as you want in offerings under Title III. The term “accredited investor” includes:

- A natural person who has individual net worth, or joint net worth with the person’s spouse or spousal equivalent, that exceeds $1 million at the time of the purchase, excluding the value of the primary residence of such person.

- A natural person with income exceeding $200,000 in each of the two most recent years or joint income with a spouse or spousal equivalent exceeding $300,000 for those years and a reasonable expectation of the same income level in the current year.

- A natural person who holds any of the following licenses from the Financial Industry Regulatory Authority (FINRA): a General Securities Representative license (Series 7), a Private Securities Offerings Representative license (Series 82), or a Licensed Investment Adviser Representative license (Series 65).

- A natural person who is a “knowledgeable employee” of the issuer, if the issuer would be an “investment company” within the meaning of the Investment Company Act of 1940 (the “ICA”) but for section 3(c)(1) or section 3(c)(7) of the ICA.

- An investment adviser registered under the Investment Advisers Act of 1940 (the “Advisers Act”) or the laws of any state.

- Investment advisers described in section 203(l) (venture capital fund advisers) or section 203(m) (exempt reporting advisers) of the Advisers Act

- A trust with assets in excess of $5 million, not formed for the specific purpose of acquiring the securities offered, whose purchase is directed by a sophisticated person.

- A business in which all the equity owners are accredited investors.

- An employee benefit plan, within the meaning of the Employee Retirement Income Security Act, if a bank, insurance company, or registered investment adviser makes the investment decisions, or if the plan has total assets in excess of $5 million.

- A bank, insurance company, registered investment company, business development company, small business ivestment company, or rural business development company

If you are not an accredited investor, Title III limits how much you can invest every year – not only in any one company, or through any one Funding Portal, but also in all companies through all Funding Portals. These limits apply only to your investments under Title III (Regulation Crowdfunding), however.

Specifically, if you are not an accredited investor the maximum amount you can invest in all Title III offerings during any period of 12 months is:

These limits are adjusted periodically by the SEC, based on inflation.

- If your annual income or net worth is less than $107,000, you may invest the greater of:

- $2,200; or

- 5% of the greater of your annual income or net worth.

- If your annual income and net worth are both at least $107,000, you can invest the lesser of:

- $107,000; or

- 10% of the greater of your annual income or net worth.

You and your spouse may combine your incomes and assets for purposes of determining how much you may invest, although if you do so, you will be treated as a single investor for purposes of determining how much either of you may invest.

EXAMPLE: Investor Smith earns $107,000 per year and has a net worth of $150,000. Investor Smith makes his first Title III investment on December 1, 2016, investing $7,500 in Company X. On November 27, 2017 Investor Smith would like to make his second Title III investment, investing $5,000 in Company Y. But he can’t; he can invest only $3,200 in Company Y. But he could invest $3,200 in Company Y on November 27, 2017 and another $1,800 (actually, another $10,700, if he wanted to) on December 1, 2017.

Title III may not be used if the Issuer or certain other people have been the subject of certain disqualifying events during the last 10 years.

The “certain other people” are:

- Any predecessor of the Issuer.

- Any director, officer, general partner, or manager of the Issuer.

- A person owning 20% or more of the Issuer’s voting power.

- Any promoter associated with the Issuer.

- Investment advisers described in section 203(l) (venture capital fund advisers) or section 203(m) (exempt reporting advisers) of the Advisers Act

- Any person who will be paid for soliciting investors; and.

- Any general partner, director, officer, or manager of such a solicitor.

The “certain disqualifying events” include a long list of events, all involving improper actions in the securities business – for example, the conviction of a felony or misdemeanor in connection with the purchase or sale of any security, or the loss of license of a securities broker for misconduct. As explained above, we will conduct background checks before allowing an Issuer to list on our Platform

Once you buy a Security (e.g., a promissory note), you aren’t allowed to sell or otherwise transfer the Security for one year, except for sales or transfers:

- Back to the Issuer;

- To an accredited investor;

- As part of an offering registered with the SEC; or

- To a family member, to a trust you control, to a trust created for the benefit of your family member, or in connection with death or divorce.

The term “family member” includes a child, stepchild, grandchild, parent, stepparent, grandparent, spouse or spousal equivalent, sibling, mother-in-law, father-in-law, son-in-law, daughter-in-law, brother-in-law, or sister-in-law of the purchaser, and includes adoptive relationships. The term “spousal equivalent” means a cohabitant occupying a relationship generally equivalent to that of a spouse.

INFORMATION THE ISSUER WILL DISCLOSE

If you make an investment commitment and there are important changes between the date of your commitment and the date the investment is concluded, then (1) the Issuer must notify you of the changes, (2) your investment commitment will be canceled automatically unless you reconfirm your commitment within five business days of receipt of the notice.

Before you invest, the Issuer must provide you with extensive information on a Form C, which will be available on the Site. The information includes:

- The Issuer’s name, address, and website

- The Issuer’s directors and officers

- The principal occupation and employment for the last three years of each director and officer

- The names of each person owning 20% or more of the Issuer’s voting securities

- The risk factors associated with the investment

- The Issuer’s business and business plan

- How the proceeds of the offering will be used

- The Issuer’s ownership and capital structure

- A description of how rights exercised by the principals of the Issuer could affect investors

- The compensation paid to us in the offering

- A description of previous offerings by the Issuer

- Whether the Issuer has previously failed to file the reports required by law

- Transactions with officers, directors, and other “insiders”

- Whether the Issuer would be disqualified from offering securities under Title III under the “bad actor” rules, if the effective date of those rules were different

- A discussion of the Issuer’s financial condition

- How the Issuer will deal with over-subscriptions

- Where on the Issuers website it will post annual reports, and when the annual reports will be available

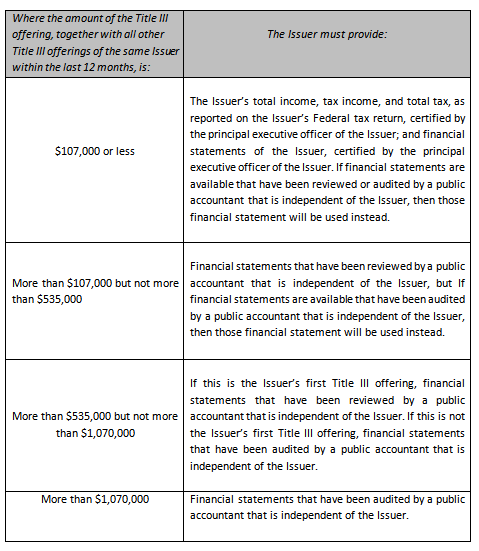

- Financial information about the Issuer, as described below

- Any “testing the waters” materials

- Any other information necessary in order to make the statements made, in light of the circumstances in which they were made, not misleading

- How much money the Issuer is trying to raise in the current offering;

- Whether this is the Issuer’s first offering using Title III; and

- If this is not the Issuer’s first offering using Title III, how much the Issuer has raised in other Title III offerings during the last 12 months.

All financial statements must be prepared in accordance with U.S. “generally accepted accounting principles.” Financial statement reviews must be conducted in accordance with the Statements on Standards for Accounting and Review Services issued by the Accounting and Review Services Committee of the AICPA. Financial statement audits must be conducted in accordance with either (i) auditing standards of the AICPA, or (ii) the standards of the Public Company Accounting Oversight Board.

After you invest, the Issuer is generally required to file annual reports with the SEC and post them on its own website within 120 days after the end of the fiscal year. The annual report will typically include:

- The same types of information included on the Form C you saw when you invested;

- Updated financial statements certified by the principal executive officer of the Issuer (the financial statements don’t have to be reviewed or audited, but if the Issuer already has reviewed or audited financial statements, they must be provided); and

- Updated disclosures about the Issuer’s financial condition.

- The date the Issuer has filed at least one annual report and has fewer than 300 shareholders of record;

- The date the Issuer has filed at least three annual reports and has total assets no greater than $10 million;

- The date the Issuer or someone else buys all of the securities issued in the Title III offering;

- The date the Issuer registers its securities and is required to file reports under the Securities Exchange Act of 1934; or

- The date the Issuer is dissolved under state law.

RISKS OF INVESTING

Risks Associated with Technology Companies: Many of the Issuers on our Platform will be in the technology industry. Investing in technology can be enormously profitable but is also very risky. Among other things:

- We know technology will continue to advance, but it is extremely difficult to predict in exactly what direction. Most new technologies never achieve commercial success.

- Competition in the technology industry is intense.

- A few companies – Google, Apple, Amazon, and Facebook – dominate the technology industry. When one of these companies announces that it intends to invest in a given technology, the announcement itself can destroy smaller companies.

- Technology changes rapidly. Nokia, now almost forgotten, was the powerhouse of telephone handset manufacturers not long ago. MySpace was a very promising company until Facebook took over the space. Within the last 12 months Zoom has lapped all its competition in the video conferencing space. One after another technology companies rise and fall. Thus, while a technology company might find quick success it can just as quickly become obsolete.

Reliance on Management: Most of the time, the securities you buy through our Platform will not give you the right to participate in the management of the company. Furthermore, if the founders or other key personnel of the issuer were to leave the company or become unable to work, the company (and your investment) could suffer substantially. Thus, you should not invest unless you are comfortable relying on the company’s management team. You will almost never have the right to oust management, no matter what you think of them.

Inability to Sell Your Investment: The law prohibits you from selling your securities (except in certain very limited circumstances) for one year after you acquire them. Even after that one-year period, a host of Federal and State securities laws may limit or restrict your ability to sell your securities. Even if you are permitted to sell, you will likely have difficulty finding a buyer because there will be no established market. Given these factors, you should be prepared to hold your investment (your promissory note) for its full term.

The Issuer Might Need More Capital: An issuer might need to raise more capital in the future to fund new product development, expand its operations, buy property and equipment, hire new team members, market its products and services, pay overhead and general administrative expenses, or a variety of other reasons. There is no assurance that additional capital will be available when needed, or that it will be available on terms that are not adverse to your interests as an investor. If the company is unable to obtain additional funding when needed, it could be forced to delay its business plan or even cease operations altogether.

Changes in economic conditions could hurt an issuer’s businesses: Factors like global or national economic recessions, changes in interest rates, changes in credit markets, changes in capital market conditions, declining employment, decreases in real estate values, changes in tax policy, changes in political conditions, and wars and other crises, among other factors, hurt businesses generally and small, local businesses in particular. These events are generally unpredictable.

No Registration Under Securities Laws: The securities sold on our Platform will not be registered with the SEC or the securities regulator of any State. Hence, neither the companies nor their securities will be subject to the same degree of regulation and scrutiny as if they were registered.

Incomplete Offering Information: Title III does not require us or the issuer to provide you with all the information that would be required in some other kinds of securities offerings, such as a public offering of shares (for example, publicly-traded firms must generally provide investors with quarterly and annual financial statements that have been audited by an independent accounting firm). Although Title III does require extensive information, as described above, it is possible that you would make a different decision if you had more information.

Lack of Ongoing Information: Companies that issue securities using Title III are required to provide some information to investors for at least one year following the offering. However, this information is far more limited than the information that would be required of a publicly-reporting company; and the company is allowed to stop providing annual information in certain circumstances.

Breaches of Security: It is possible that our systems would be “hacked,” leading to the theft or disclosure of confidential information you have provided to us. Because techniques used to obtain unauthorized access or to sabotage systems change frequently and generally are not recognized until they are launched against a target, we and our vendors may be unable to anticipate these techniques or to implement adequate preventative measures.

Uninsured Losses: A given company might not buy enough insurance to guard against the risks of its business, whether because it doesn’t know enough about insurance, because it can’t afford adequate insurance, or some combination of the two. Also, there are some kinds of risks that are simply impossible to insure against, at least at a reasonable cost. Therefore, any company could incur an uninsured loss that could damage its business.

The Owners Could Be Bad People or Do Bad Things: Before we allow a company on our Platform, we run certain background checks, including criminal background checks. However, there is no way to know for certain that someone is honest, and even generally honest people sometimes do dishonest things in desperate situations – for example, when their company is on the line, or they’re going through a divorce or other stressful life event. It is possible that the management of a company, or an employee, would steal from or otherwise cheat the company, and you.

Unreliable Financial Projections: Issuers might provide financial projections reflecting what they believe are reasonable assumptions concerning their businesses. However, the nature of business is that financial projections are rarely accurate, not because issuers intend to mislead investors but because so many things can change, and business is so difficult to predict.

Limits on Liability of Company Management: Many companies limit the liability of management, making it difficult or impossible for investors to sue managers successfully if they make mistakes or conduct themselves improperly (not all liability can be waived, however). You should assume that you will never be able to sue the management of any company, even if they make decisions you believe are plainly wrong.

Changes in Laws: Changes in laws or regulations, including but not limited to zoning laws, environmental laws, tax laws, consumer protection laws, securities laws, antitrust laws, and health care laws, could adversely affect many companies.

Conflicts of Interest with Us: In most cases, we make money as soon as you invest. You, on the other hand, make money only if your investments turn out to be successful. Or to put it a different way, at least in the short term it is in our interest to have you invest as much as possible in as many companies as possible, even if they all fail and you lose your money.

Conflict of Interest with Companies and their Management: In many ways your interests and the interests of company management will coincide: you both want the company to be as successful as possible. However, your interests might be in conflict in other important areas, including these:

·You might want the company to distribute money, while the company might prefer to reinvest it back into the business.

·You might wish the company would be sold so you can realize a profit from your investment, while management might want to continue operating the business.

·You would like to keep the compensation of managers low, while managers want to make as much as they can.

Lack of Professional Advice: Because of the limits imposed by law, you might invest only a few hundred or a few thousand dollars in a given company. At that level of investment, you might decide that it’s not worthwhile for you to hire lawyers and other advisors to evaluate the company. Yet if you don’t hire advisors, you are in many respects “flying blind” and more likely to make a poor decision.

Your Interests Aren’t Represented by Our Lawyers: We have lawyers who represent us, and most of the companies on the Platform also have lawyers, who represent them. These lawyers have drafted the Terms of Use and Privacy Policy on the Site, and will draft all the documents you are required to sign. None of these lawyers represents you personally. If you want your interests to be represented, you will have to hire your own lawyer, at your own cost.

Future Investors Might Have Superior Rights: If the company needs more capital in the future and sells stock to raise that capital, the new investors might have rights superior to yours. For example, they might have the right to be paid before you are, to receive larger distributions, to have a greater voice in management, or otherwise.

Our companies will not be subject to the corporate governance requirements of the national securities exchanges: Any company whose securities are listed on a national stock exchange (for example, the New York Stock Exchange) is subject to a number of rules about corporate governance that are intended to protect investors. For example, the major U.S. stock exchanges require listed companies to have an audit committee made up entirely of independent members of the board of directors (i.e., directors with no material outside relationships with the company or management), which is responsible for monitoring the company’s compliance with the law. Companies listed on our Platform typically will not be required to implement these and other stockholder protections.

Many of the Securities listed on our Platform are speculative and involve significant risk, including the risk that you could lose some or all of your money. We’re describing some of the factors that make these investments risky in four ways:

- First, because many of the opportunities on our Platform will be in small businesses, we’ll describe risks common to those businesses.

- Second, we’ll describe risks common to most of the businesses on our Site.

- Third, we'll describe risks associated with equity securities, debt securities, revenue-sharing notes, and SAFEs.

- Fourth, when you review a particular investment opportunity, the Issuer will also provide a list of risks specific to that opportunity.

Lack of Professional Management: Most small companies are managed by their founders. Very often the founder of a company is very strong in one area – for example, she might be an extremely effective salesperson or a terrific baker – but lacks experience or skills in other critical areas. It might be a long time before (1) a startup can afford to hire professional management, and (2) the founder recognizes the need for professional management. In the meantime, the company and its investors could suffer.

Lack of Access to Capital: Small companies have very limited access to capital, a situation that Title III Funding Portals hope to improve but cannot fix entirely. Frequently these companies cannot qualify for bank loans, leaving the company to live off the credit card debt incurred by the founder. Capital is the oxygen of any business, and without it a business will eventually suffocate and fail.

Limited Products and Services: Most small businesses sell only one or two products or services, making them vulnerable to changes in technology and/or customer preferences.

Lack of Accounting Controls: Larger companies typically have in place strict accounting controls to prevent theft and embezzlement. Smaller companies typically lack these controls, exposing themselves to additional risk.

Lack of Technology: Many small businesses cannot afford the technology that a larger business would use to create efficiencies and cost savings.

Cash Flow Shortfalls: Many small businesses experience frequent shortfalls in cash flow. If a business doesn’t have enough money to meet payroll, it might not make payments on obligations to its investors, either.

Competition: A small business is likely to be vulnerable to competition, whether in the form of another small business or a national chain.

You Have a Limited Upside: As a creditor of the company, the most you can hope to receive is your money back plus interest. You cannot receive more than that even if the company turns into the next Facebook.

You Do Have a Downside: Conversely, if the company loses enough value, you could lose some or all your money.

Subordination To Rights Of Other Lenders: Typically, when you buy a debt security on our Platform, while you will have a higher priority than holders of the equity securities in the company, you will have a lower priority than some other lenders, like banks or leasing companies. In the event of bankruptcy, they would have the right to be paid first, up to the value of the assets in which they have security interests, while you would only be paid from the excess, if any.

Lack of Security: Sometimes when you buy a debt security on our Platform, it will be secured by property, like an interest in real estate or equity. Other times it will not.

Lack of Guaranty: Sometimes when you buy a debt security on our Platform, it will be guaranteed by the owner of the business, or by someone else. Other times it will not.

Issuers typically will not have third party credit ratings: Credit rating agencies, notably Moody’s and Standard & Poor’s, assign credit ratings to debt issuers. These ratings are intended to help investors gauge the ability of the issuer to repay the loan. Companies on our Platform generally will not be rated by either Moody’s or Standard & Poor’s, leaving investors with no objective measure by which to judge the company’s creditworthiness.

Interest Rate Might Not Adequately Compensate You for Risk: Theoretically, the interest rate paid by a company should compensate the creditor for the level of risk the creditor is assuming. That’s why consumers generally pay one interest rate, large corporations pay a lower interest rate, and the Federal government (which can print money if necessary) pays the lowest rate of all. However, the chances are very high that when you lend money to a company on the Platform (buying a promissory note is the same as lending money), the interest rate might not compensate you adequately for the level of risk.

Equity Comes Last in the Capital Stack: The holders of the equity interests stand to profit most if the company does well, but stand last in line to be paid when the company dissolves. Everyone – the bank, the holders of debt securities, even ordinary trade creditors – has the right to be paid first. You might buy equity hoping the company will be the next Facebook, but face the risk that it will be the next Theranos.

In Most Cases, You Will Be A Minority Investor: Investors will typically be “minority” owners of companies on the Platform, meaning that other parties will have complete voting and managerial control over the company. As a minority stockholder, you typically will not have the right or ability to influence the direction of the company. You will generally be a passive investor. In some cases, this may mean that your securities are treated less preferentially than those of larger security holders.

Possible Tax Cost: Many of the companies on the Platform will be limited liability companies. In almost every case these limited liability companies will be taxed as partnerships, with the result that their taxable income will “flow through” and be reported on the tax returns of the equity owners. It is therefore possible that you would be required to report taxable income of a given company on your personal tax return, and pay tax on it, even if the company doesn’t distribute any money to you. To put it differently, your taxable income from a limited liability company is not limited to the distributions you receive.

Your Interest Might Be Diluted: As an equity owner, your interest will be “diluted” immediately, in the sense that (1) the “book value” of the company is very likely to be lower than the price you are paying, and (2) the founder of the company, and possibly others, bought their stock at a lower price than you are buying yours. Your interest could be further “diluted” in the future if the company sells stock at a lower price than you paid.

Future Investors Might Have Superior Rights: If the company needs more capital in the future and sells stock to raise that capital, the new investors might have rights superior to yours. For example, they might have the right to be paid before you are, to receive larger distributions, to have a greater voice in management, or otherwise.

Dilution of Voting Rights: Even if you have any voting rights to begin with (and many of the equity securities offered on the Platform will have no voting rights), these rights will be diluted if the company issues additional equity securities.

You Have a Limited Upside: Although a revenue-sharing note has more upside than a standard note, the upside is still limited.

Revenue is Uncertain: The amount and timing of a company’s revenues can be extremely hard to predict. For example, the management of an Issuer might make decisions they believe will lead to a higher value for the company, but also lead to lower revenue, at least in the short term. In fact, companies like Facebook have achieved extremely high valuations before they achieved significant revenue.

Arbitrary Terms: The terms of your revenue-sharing notes – for example, whether your maximum payout is 1.5 times your investment, 2.0 times your investment, or something else – were likely set by management on an arbitrary basis, without regard to traditional measures of value like profitability.

Conflicts with Management: As the holder of a revenue-sharing note your interests could conflict with the interests of management in terms of the timing of revenue recognition.

Other Risks of Debt Securities Apply: All the risks listed above for debt securities also apply to revenue-sharing notes.

You Don’t Know What You’re Getting: You don’t know what your SAFE is worth when you buy it. Indeed, this is why SAFEs were invented in the first place – to avoid the need to place a valuation on a small company.

SAFEs are not Appropriate for all Issuers: SAFEs were developed in Silicon Valley for a particular kind of common that is common in Silicon Valley: a company expected to experience rapid growth and multiple rounds of financing with an exit (a sale of the company or a public offering) in the not-too-distant future. Of all the companies formed in the U.S. every year, only a small percentage fit that profile. Consequently, SAFEs are not always appropriate.

Other Risks of Equity Securities Apply: All the risks listed above for equity securities also apply to SAFEs.

SECURITIES

An Issuer might hire a public relations firm or other third party to promote the Issuer’s offering on the Platform – for example, by talking about the offering in our chat room. Or an employee or founder of the Issuer might do the same thing. In either case, the person doing the promoting must identify himself or herself on the Platform and disclose that he or she is engaged in promotional activity. In the case of a third party, the third party must also disclose that it is being paid for its promotional activity.

The SEC recently approved changes to Title III, including changes that:

- Allow accredited investors to invest any amount, with no limits.

- Raise the investment limits for non-accredited investors.

- Raise the amount an Issuer may raise, to $5M per year.

- Limit the kinds of Securities that may be issued.

We expect to offer various kinds of Securities on our Platform:

- Debt Securities – Specifically, promissory notes. The promissory notes will require the Issuer to pay your money back, plus interest at a specified rate, over a specified time period. Owning a promissory note does not make you an owner of the company. Instead, you are a creditor. As long as the company has enough money to repay your loan, plus any interest you’ve been promised, the value of your security stays the same; the fluctuations of the fortunes of the company don’t affect you, unless the fortunes go way down. On the other hand, you don’t share in the appreciation if things go well. If the company increases in value 100-fold, you just have the right to get your money back, plus interest.

- Revenue-Sharing Notes – A regular promissory note requires the Issuer make specified payments of interest and principal at specified times. In contrast, a revenue-sharing note requires the Issuer to pay a specified percentage of its revenue. For example, a revenue-sharing note might require the Issuer to pay investors 5% of its revenue for four years. Typically, a revenue-sharing note will also state a maximum that investors are entitled to receive (e.g., double their investment) and a due date for repayment of the original investment.

- Equity Securities – When you buy an “equity security,” like the common stock of a corporation, you become an owner of the company. The value of your interest fluctuates with the fortunes of the company; if the company does well the value of your interest goes up, while if it does poorly the value goes down, possibly all the way to zero. As an owner, you generally have the right to share in any profit distributions made by the company, and you also share in the appreciation in the value of the company. Owning an equity security in a company is like owning a house, both the good part and the bad part. When a company dissolves, the owners of the equity securities are paid last, after all the creditors.

- “Preferred” Equity Securities – In some cases, a company will offer a “preferred equity security,” like the preferred stock of a corporation. Typically, the holders of the preferred equity security have a right to receive distributions before the holders of the regular equity securities. For example, the holders of a preferred stock might have the right to receive a 4% dividend before dividends are paid to the holders of common stock. But preferred equity is still equity. The holders of preferred equity are paid after creditors.

- Hybrid Securities – Some securities, which we call “hybrid securities,” have characteristics of both equity securities and debt securities, like a cross between a dog and a horse.

- Convertible Securities – Some securities, which we call “convertible securities,” start out as one kind of security but can be changed – converted – into a different kind of security. For example, a company might issue a debt security that can be converted by the holder into common stock at some specified time. Sometimes the conversion is triggered at the option of the holder, sometimes at the option of the company, and other times upon the occurrence of a specified event.

- SAFEs – “SAFE” stands for “simple agreement for future equity.” Although there are many kinds of SAFEs, the typical SAFE converts into an equity security – either common stock or preferred stock – when the Issuer raises more money in the future. If the Company never raises more money in the future you typically have to wait until the company is sold or dissolved to get your money back.

- Callable Securities – Any kind of security can also be a “callable security,” meaning it can be “called,” or redeemed (bought back) by the company (for a debt security this is equivalent to an issuer having the option to prepay a loan prior to its maturity).

- Other Kinds of Securities – The possible kinds of securities are limited only by the imaginations of financial needs of companies, investors, and lawyers.